In September, the liquidity is expected to be a risk-free fund, and there are three hurdles.

There are three hurdles in the funds clearance China Securities Journal â–¡ reporter Wang Wei "The exchange overnight interest rate rushed to 8%!" On the morning of the 30th, brokerage trader Xiao Li stared nervously at the disk. Since August, the funds have been almost from the beginning of the month to the end of the month. Many traders, especially those like Xiao Li, who are in non-bank institutions, have to “seek†funds everywhere, and the “legends†of institutional defaults have also reappeared. Fortunately, on the 30th, the supply of funds increased, and the liquidity tightened slightly. Xiao Li also successfully flattened his position. However, the most difficult time is probably not yet coming. It will enter the end of the season, the maturity of the interbank deposits exceeds 2 trillion, the MPA assessment at the end of the quarter, and the impact of the external currency environment will be the three hurdles for the smooth “customs clearanceâ€. Analysts pointed out that in the context of the low reserve ratio, the recent large-scale withdrawal of central bank funds has made the organization "people's heart", coupled with a lot of disturbance factors in September, market liquidity expectations are difficult and difficult, but in the central bank Under the operational tone of “Feng Shi Gu Guâ€, there is no need to worry too much about the liquidity in September. Resurgence of funds At the end of August, traders like Xiao Li once again entered the state of “begging overnightâ€. Since the 25th, the short-term repo rate of the exchange has started to rise, which visually shows the difficulty of financing and financing of non-bank institutions. On the morning of the 30th, the central bank's open market operation (OMO) once again returned 100 billion yuan, which aggravated market tension. The overnight interest rate of the Shanghai Stock Exchange overnight was up to 8.15%. The cross-monthly 7-day GC007 interest rate also touched 6.14%. The high point, both hit a new high since the end of July. "You can't do anything about it. To flatten your position, you have to take your head and take it!" Xiao Li said. According to industry sources, on the previous day (29th), there were still a few institutions that did not close their positions in the late stage. Since August, the funds have been almost from the beginning of the month to the end of the month, and the interest rate of funds has been rising all the way. This situation clearly exceeds market expectations. From the perspective of the interbank money market, the closing price on the 29th, overnight weighted interest rate (DR001 reported 2.9226%, compared with the early low of 2.61616 up 30BP; 7-day weighted interest rate (DR001) reported 2.9322%, compared with the early low of 2.7838% up 15BP . The industry generally believes that in the context of a low reserve ratio, taxation, payment, government bond issuance and other disturbance factors are superimposed, while the central bank's OMO is weaker than in July, especially in the near future. As a result, the funds face unexpectedly tight. “As the ultra-reserve rate continues to be at a lower level, the funding of the banking system is more fragile, and the impact of the cyclical liquidity of the central bank’s open market operations on the market capital is even more pronounced.†Chief Analyst of CITIC Securities Clearly pointed out. According to Wind data, in the 22 trading days ending August 30, the central bank's open market operations had a net return of 11 trading days, and there were 6 trading days to achieve neutral hedging, with only 5 trading days to achieve net delivery. In general, in August, the central bank carried out a reverse repurchase operation of 263 billion yuan, and the reverse repurchase expired at 3.11 billion yuan; the MLF operation was 399.5 billion yuan, and the MLF expired 287.5 billion yuan; the accumulated net withdrawal fund of the month was 368 billion yuan. Analysts pointed out that although fiscal expenditures, treasury deposit operations, financial institutions' statutory reserve withdrawals and other factors have formed liquidity supply, the recent open market funds have more net withdrawals, the market's overall over-reserve rate is low and the liquidity distribution is uneven. Other factors have limited the liquidity to warm up, superimposed on the influence of the end of the month, the financial institutions are cautious, and the capital fabrics are cross-monthly in a tightly balanced pattern. There are also three hurdles in September. On the 30th, with the support of increased fiscal expenditure at the end of the month, the tightness of funds in the afternoon eased slightly. The overnight weighted interest rate DR001 fell 4BP to 2.92%, and the index 7-day weighted interest rate DR007 also fell nearly 6BP to 2.885. But thinking that it is about to enter September, Xiao Li is not optimistic. “The most difficult time may not have arrived yet.†Industry insiders pointed out that in the context of the low reserve rate, the expiration of the same-day inventory in September, the end of the quarter-end MPA assessment, and the impact of the external monetary environment will be followed. The three sides of the funds have to face. First of all, compared with March, June and September, the expiration of interbank deposits reached a record high, which will put a lot of pressure on the interest rate of funds. This is also the focus of the current market. In June, the central bank relaxed its margins on liquidity. After the funds were relatively loose, small and medium-sized commercial banks issued a large number of interbank certificates of deposit. The largest proportion of them was the three-month maturity deposit receipts. These interbank certificates of deposit faced a large number in September. period. According to statistics, the amount of inter-bank deposits due in September was 2.3 trillion yuan, exceeding the level of January-August this year. There is a large pressure for continuous rolling. At the end of September, the pressure on the MPA assessment is higher. Upside pressure. Secondly, historically, the liquidity assessment pressures such as MPA and LCR at the end of the quarter will have a contraction effect on bond investment, bank and non-bank asset management cooperation and inter-bank repurchase, which will easily lead to tight funding. Since the beginning of this year, the bank's excess reserve ratio has remained at a historically low level. The MPA assessment is approaching, and the superposition of interbank deposit certificates will expire, which will lead to further increase in bank liquidity pressure. According to the agency's calculations, the excess reserve ratio of financial institutions has dropped to around 1.1% at the end of July. After paying taxes in mid-August, it may fall further to 1%, which is a very low level in history. In addition, the impact of the interbank deposit receipts in the MPA assessment and the new rules of the monetary fund on the liquidity in the history remains to be seen. In addition, in September, the Fed may also announce the start of “shrinking the tableâ€, the euro zone monetary policy also tightened expectations, and the external monetary environment may also have a certain impact on domestic liquidity. Changjiang Securities pointed out that the Fed FOMC meeting held at the end of each season may also interfere with domestic liquidity. In general, in the context of maintaining a low level of ultra-reserve ratio, the banking system is fragile, and there are many liquidity disturbance factors in the upcoming September. The market liquidity expectation is difficult and difficult. Don't worry too much Although the “three hurdles†have caused certain obstacles to the liquidity operation, market participants also believe that the tone of the central bank’s monetary policy has not changed, and the currency operations of “not loose and tight†and “shaving the peaks and filling the valley†Next, there is no need to worry too much about the liquidity environment in September, and the probability of funding will remain tight. The Yangtze River Securities Research Report pointed out that in September, the maturity of interbank deposit receipts reached a record high, and it also faced the impact of MPA assessment and Fed FOMC meeting. Compared with the end of the first two quarters, the liquidity environment in September should not be too worried or too high. Money issuance or continue to "cut the peaks and fill the valley", maintain the basic stability of the liquidity of the banking system, maintain a tight balance of funds, still need to do a good job of liquidity management. Analysts at CICC said that the rolling issue of interbank deposits in September would be frictionally caused by a rematch between supply and demand, especially as banks would increase their reserves due to uncertainty. Coupled with the MPA assessment at the end of the season, LCR and other liquidity assessment pressures, it is easy to trigger pressure on the funds. However, from the actual situation this year, the market is generally worried about the quarterly market. However, due to the central bank’s fund-raising operation and the concentrated placement of fiscal deposits at the end of the quarter, the funds are not nervous. Under the unfettered monetary policy and the operation of cutting the peaks and filling the valley, the large probability of funds is still in danger. It is clear that the funds will be relatively abundant in September. First of all, the new rules of the IMF are not clear, the cargo base continues to be more efficient in interbank deposits, and the maturity risk is lower. Secondly, based on the release ratio of fiscal deposits at the end of the third quarter of 2015 and 2016, the estimated release in September is estimated. Between 500 billion yuan and 900 billion yuan, the funds are abundant; in the context of low reserve ratios, the central bank adopted pre-adjustment through pre-judgment, so that the liquidity cycle is opposite to the market expected funding period. "It is not loose." In mid-September, the central bank will start a net liquidity release to ensure that the funds at the end of September are "not tight." From the perspective of comprehensive institutions, the low reserve ratio means that the funds are “smoothâ€, and there are many disturbance factors in September. The fluctuation of funds will be inevitable, but the central bank’s monetary policy remains stable and neutral, and the open market operation “cuts the peaks and fills the valleyâ€. It is still normal for the follow-up funds to remain tight and maintain a tight balance. Enter [Sina Finance and Economics Unit] Discussion Glasses With Magnetic Sunglasses The hot summer hits, and the sun begins to be unrestrained. When myopia meets the glare of the sun, how to choose between myopia glasses and sunglasses? BELIEYE magnetic sunglasses easily solve the worries of myopic people! Myopia glasses 1s turns into Sun Glasses! It can be done indoors and outdoors.

â— The magnets of BELIEYE magnetic sunglasses have the characteristics of low presence and high functionality, and the short-sighted glasses can be changed into sunglasses with a single tap.

Glasses With Magnetic Sunglasses,Magnetic Clip on Sunglasses,Magnetic Sunglasses,Eyeglasses with Magnetic Sunglasses Belieye (Jiangsu) Co.,LTD , https://www.believeglasses.com![]() Yinhua Cup Top Ten Banking Planner Contest, Surprise Awards High Honor is waiting for you!

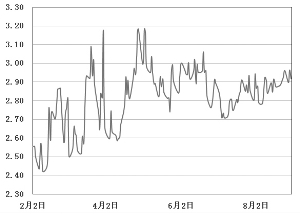

Yinhua Cup Top Ten Banking Planner Contest, Surprise Awards High Honor is waiting for you!  Interbank market 7-day repo rate (DR007) trend

Interbank market 7-day repo rate (DR007) trend

â— The lenses of BELIEYE magnetic sunglasses use TAC polarized lenses, which can effectively filter out glare, so that you can travel worry-free whether you are driving or traveling.

â— Whether you are concentrating on work or embracing life comfortably, BELIEYE magnetic sunglasses make you so attractive in every way.